A World in Need of More Gas Isn’t Getting New Supply Fast Enough

(Bloomberg) -- A wave of new liquefied natural gas supply from projects agreed years ago in anticipation of surging demand keeps getting pushed back, threatening to extend the global energy crisis.

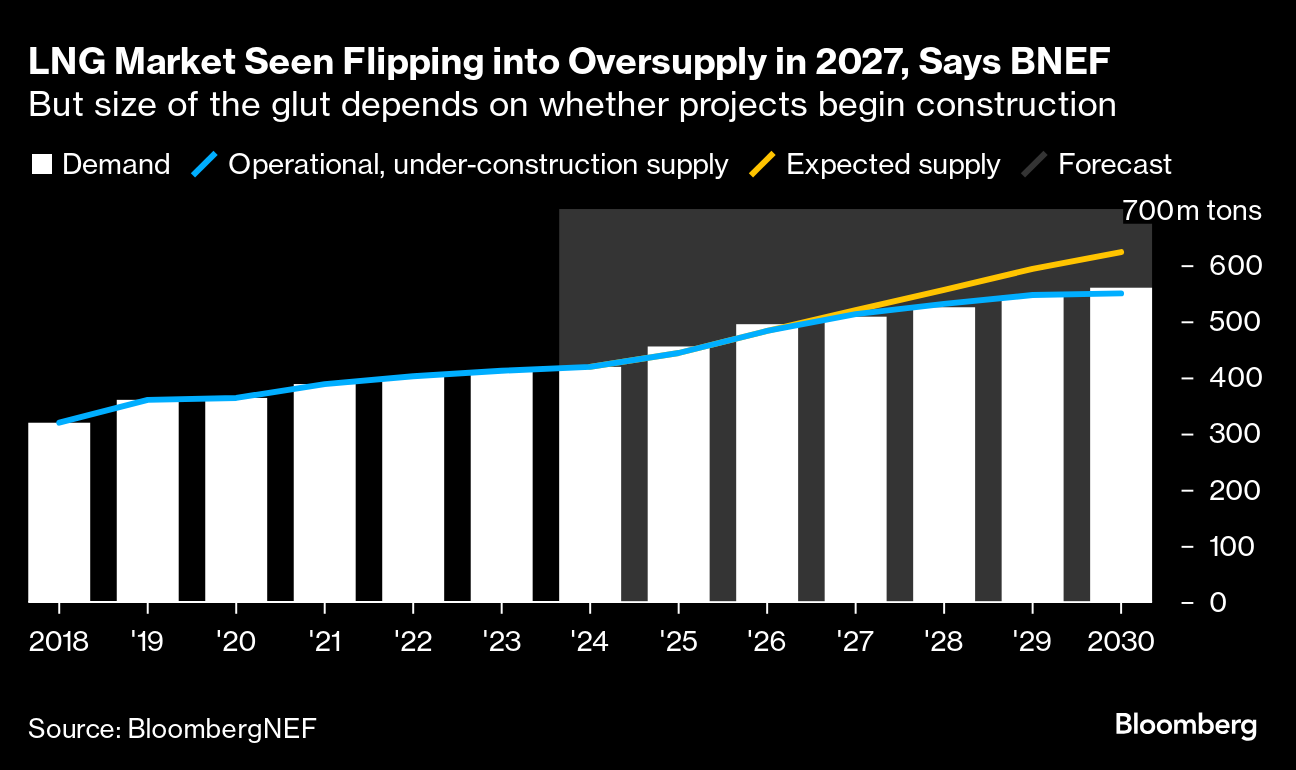

Delays from the US to Mozambique promise little imminent relief from high fuel prices, despite more than $200 billion in investments that were supposed to flip the LNG market into oversupply as early as 2025.

For some countries, new sources of gas couldn’t come fast enough. Germany hasn’t seen two consecutive quarters of growth since before the energy crisis sent its manufacturers tailspinning. And while Europe saw two exceptionally mild winters in recent years, the colder temperatures that are predicted for some areas this season could intensify competition with Asia for the fuel, triggering shortages for nations that can’t afford it.

“The market is trying to build an unprecedented amount of new capacity in a short time frame. That’s not easy to pull off,” said Ira Joseph, a fellow at the Center on Global Energy Policy at Columbia University.

There are several reasons for the delays, including extended construction at liquefaction projects in Texas and Mexico, as well as western sanctions holding back Russia’s Arctic LNG 2 plant. At the same time, global demand is rising and new buyers are entering the fray, with Egypt becoming a net importer this year after facing production issues and an extremely hot summer.

Consumption will probably be higher next year than in 2024, in part driven by a gradual shift to gas in the power and transport sector in Asia, said Florence Schmit, an energy strategist at Rabobank. Any additions to supply in the second half of 2025 might come too late to catch up with the increased demand, she added.

The International Energy Agency pared back its outlook for LNG production gains in 2025 in an update last week. Global output will climb to just shy of 580 billion cubic meters in 2025, it said in a quarterly report, down from a previous prediction of more than 600 billion cubic meters.

Relief will also be limited the following year, according to research firm Wood Mackenzie Ltd., which trimmed estimates for extra supply by about 16% from calculations made six month ago.

“This is still a sizeable annual increase, so downward price pressure remains a key theme for 2026,” said Lucas Schmitt, an analyst at WoodMac. “However, delays have made the expected price drop less pronounced than earlier in the year.”

While the current cost of gas has come down substantially from the peaks seen in 2022, benchmark futures in Europe are still about twice as high as before the crisis, when Russia curbed pipeline flows to the region. An increased reliance on LNG is partially to blame, as Europe now competes with buyers from around the world and fuel goes to the highest bidder.

What’s more is that demand for LNG is expected to go up substantially by the end of the decade as the artificial intelligence boom raises needs for power-hungry data centers. McKinsey & Co. sees AI requirements making up 5% of Europe’s power needs by 2030, while BlackRock expects energy consumption across Asia Pacific to increase by about 50% in the next 10 years. US power-sector demand for gas could rise as much as 30% by 2030 from today’s levels, according to Bloomberg Intelligence.

“We haven’t seen much in the way of LNG supply growth, but demand for LNG has been rising,” Mark Simons, head of gas and power origination at TotalEnergies SE, said at a recent conference in London. The market is “reasonably tight, and as a consequence, European prices are high, as traders are worried about what that will be like in winter.”

The US, one of Europe’s top LNG suppliers, is unlikely to add many more export facilities beyond the current slate of approved projects due to rising construction costs and regulatory challenges, from Biden’s LNG permitting pause to courts yanking permits.

Another big producer, Qatar, is set to lift exports by more than 80% by 2030, but is still a couple of years away from producing the first extra drops of fuel.

Smaller suppliers are also facing headwinds. Attacks by an Islamic State-backed insurgency has halted a major project in Mozambique. Efforts to boost output out of Papua New Guinea and Nigeria have also faltered, while some older global facilities face production declines.

For global traders such as TotalEnergies, which is involved in global LNG projects from the US to Australia to Angola, that means a longer period of elevated prices that support trading profits.

“It’s a good market like it is today,” TotalEnergies Chief Executive Officer Patrick Pouyanne said, referring to current levels of gas prices.

But for the world's developing nations, it means competing with wealthier countries for expensive fuel cargoes. A surge in prices could hamstring efforts by countries like Pakistan and Thailand to secure shipments needed to feed the economy. Malaysia and Indonesia are also set to enter the market as net importers as they run out of reserves.

“If demand continues to strengthen, driven by improving macro conditions and new demand nodes like from data centers, then any oversupply in 2027 and 2028 could evaporate completely,” said Saul Kavonic, an energy analyst at Sydney-based research firm MST Marquee.

©2024 Bloomberg L.P.