Stocks Get Tech Boost at Start of Big Jobs Week: Markets Wrap

(Bloomberg) -- A rally in the world’s largest tech companies drove stocks toward fresh all-time highs, with traders bracing for a barrage of economic data and remarks from Federal Reserve speakers that will help shape the outlook for interest rates.

Equities continued to plow ahead, with the S&P 500 poised for its 54th closing record this year and the Nasdaq 100 rising more than 1%. Tesla Inc. rallied 3.5% on bullish analyst comments while Apple Inc. hit a fresh peak. Intel Corp. climbed on news Chief Executive Officer Pat Gelsinger is leaving the job after the chipmaker’s turnaround sputtered.

Even after the strongest rally since the early days of the dot-com boom, the S&P 500 still has room to push higher, according to JPMorgan Chase & Co.’s Andrew Tyler. He says the most popular options trades are wagering the benchmark will hit 6,200 to 6,300 this month, implying a further advance of as much as 4% before the year is over, based on Friday’s close.

This week’s calendar is set to deliver a slew of key data, with Friday’s payrolls report expected to show US hiring jumped in November after hurricanes and a major strike undercut job growth a month earlier. On Wednesday, Fed Chair Jerome Powell participates in a moderated discussion, and investors will await any assessment of the job market and inflation as well as clues to whether the central bank will lower rates in December.

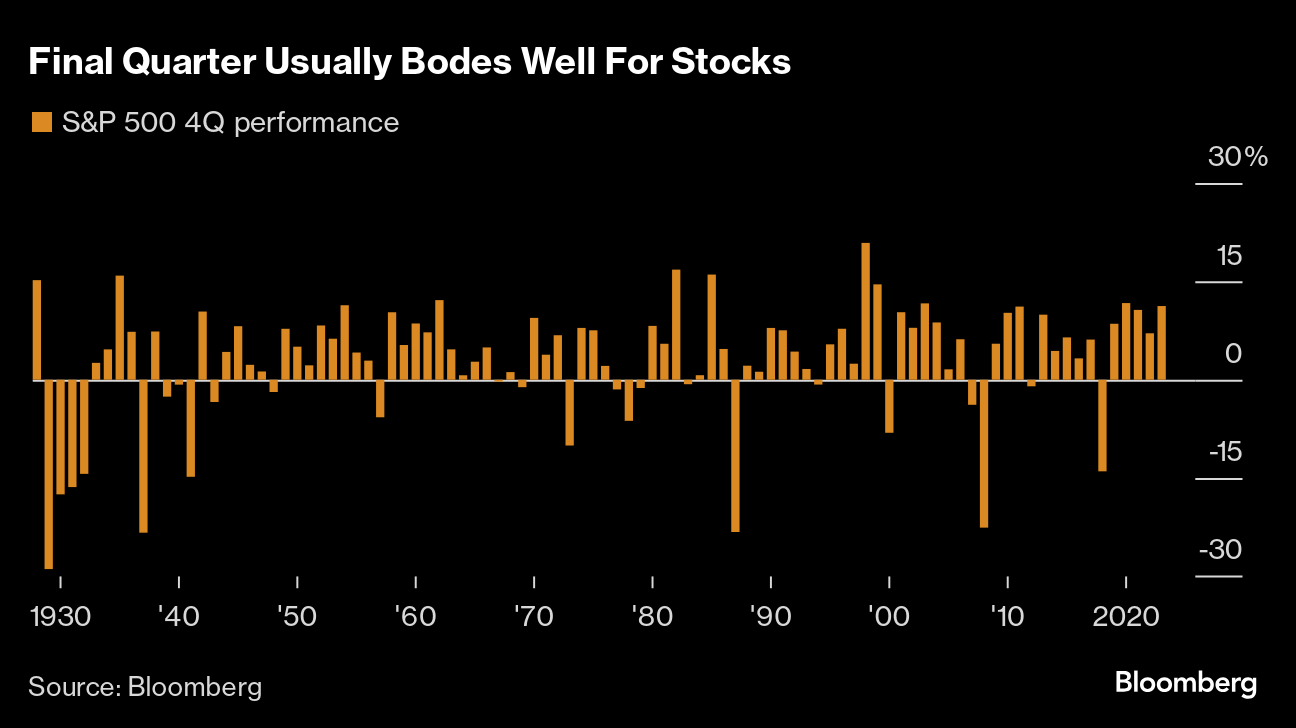

“This week is the last truly important economic data week of 2024,” said Tom Essaye at The Sevens Report. “If results are Goldilocks, then investors will expect a soft landing and a December rate cut. That will keep positive seasonals in place for a year-end grind higher.”

The S&P 500 added 0.2%. The Nasdaq 100 rose 1.1%. The Dow Jones Industrial Average fell 0.3%.

Treasury 10-year yields advanced three basis points to 4.19%. The dollar snapped a three-day losing streak amid a currency warning to BRICS nations by President-elect Donald Trump. French bonds and stocks came under renewed pressure after Marine Le Pen pledged to topple Prime Minister Michel Barnier’s government after he failed to meet her demands on a new budget.

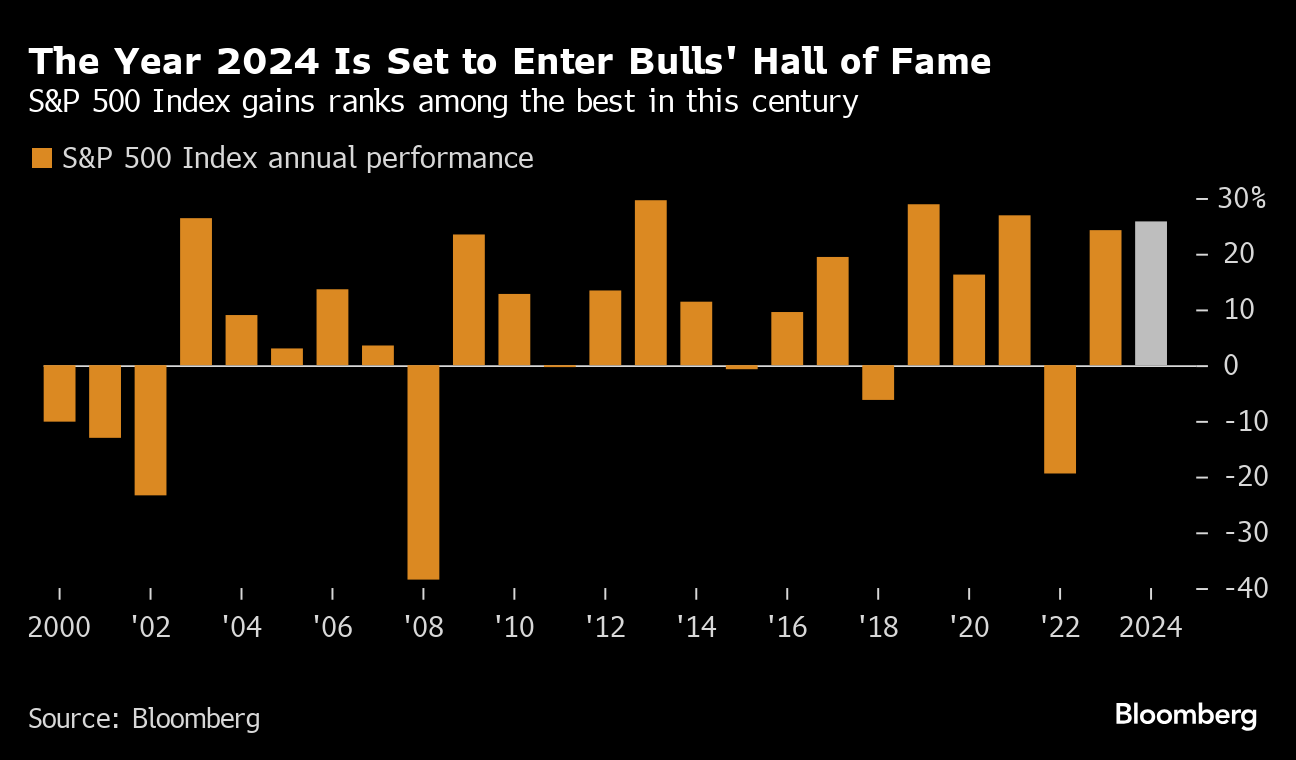

A year ago, equity investors and strategists braced for a potentially turbulent 2024, worrying about the risk of a hard landing for the US economy and rate cuts that could come too late to prevent it. Heading into the year, few anticipated that the S&P 500’s annual gain would be among the best in history.

The S&P 500 is on pace for back-to-back years with 25% returns for just the second time on record — with 1954 and 1955 posting respective gains of 53% and 33%, according to Mark Hackett at Nationwide.

“We now find ourselves in the middle of this ‘Goldilocks’ zone, where economic health supports earnings growth while remaining weak enough to justify potential Fed rate cuts,” he said. “December continues the seasonal tailwind, historically delivering the second-best performance behind November. Other technical tailwinds for the market include financial conditions, sentiment, momentum, and breadth.”

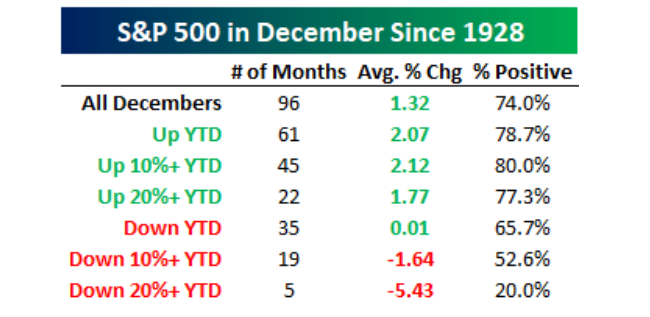

To Sam Stovall at CFRA, after the big November gains, investors still have much to look forward to.

Since World War II, he says the S&P 500 returns in December recorded: 1) the second highest average monthly return 2) the greatest frequency of advance and 3) the lowest standard deviation of returns, which during election years has been nearly 40% below the average for the 11 other months of the year.

December has usually been a stronger month when the market enters the month up solidly year-to-date, according to Bespoke Investment Group.

In the 22 years that the S&P 500 has been up more than 20% in the year through November, the index has averaged a gain of 1.77% in December — with positive returns 77.3% of the time, Bespoke noted.

“The trends in the equity market remain constructive,” said Craig Johnson at Piper Sandler. “We expect a continued broadening into SMID-caps, which should be a rising tide that lifts all boats.”

Small- and mid-cap stocks have the potential to deliver double-digit gains next year under a best-case scenario, although “a lot can go wrong,” according to JPMorgan Chase & Co. strategists including Eduardo Lecubarri.

The group is heavily under-owned after three years of record cumulative outflows, while valuations show an above-average discount to large caps, they wrote. The relative fundamental picture for small- and mid-caps no longer faces headwinds such as rising rates and wages.

The strategists also noted that Trump’s election victory also serves as a catalyst as investors are likely to prefer domestic exposure.

Corporate Highlights:

- Super Micro Computer Inc. said an independent review of its business found no evidence of misconduct but recommended that the server maker appoint new top financial and legal leadership.

- MicroStrategy Inc. sold 3.7 million shares over the past week and used the proceeds to buy another $1.5 billion worth of Bitcoin, the fourth consecutive weekly purchase announced by the crypto hedge fund proxy.

- Cloudflare Inc. was upgraded by Morgan Stanley, which said the software maker can “sustain, if not accelerate, topline growth over the next few years.”

- Core Scientific Inc. intends to offer $500 million in convertible notes via a private offering.

- Gap Inc. was upgraded at JPMorgan Chase & Co., which said the foundation has been set to support a “consistent playbook of improved merchandising and marketing.”

- Roughly 66,000 Volkswagen AG workers across Germany abandoned their posts on Monday, the first wave of temporary walkouts triggered by a stalemate over how to slash costs at the carmaker’s namesake brand.

- Stellantis NV Chief Executive Officer Carlos Tavares’s surprise departure leaves the maker of Jeep SUVs and Peugeot cars without clear leadership at a time of significant upheaval in the industry.

- Toast Inc. was downgraded at Goldman Sachs Group Inc., which cited an elevated valuation following a recent rally.

- Upstart Holdings Inc. was downgraded at JPMorgan Chase & Co., a move that’s based on valuation as shares appear to be “priced for perfection.”

Key events this week:

- Fed’s Adriana Kugler and Austan Goolsbee speak, Tuesday

- Eurozone S&P Global Eurozone Services PMI, PPI, Wednesday

- US factory orders, US durable goods, Wednesday

- Fed’s Jerome Powell and Alberto Musalem speak, Wednesday

- Fed’s Beige Book, Wednesday

- Eurozone retail sales, Thursday

- US initial jobless claims, Thursday

- Eurozone GDP, Friday

- US jobs report, consumer sentiment, Friday

Some of the main moves in markets:

Stocks

- The S&P 500 rose 0.2% as of 1:11 p.m. New York time

- The Nasdaq 100 rose 1.1%

- The Dow Jones Industrial Average fell 0.3%

- The MSCI World Index rose 0.2%

Currencies

- The Bloomberg Dollar Spot Index rose 0.6%

- The euro fell 0.9% to $1.0487

- The British pound fell 0.7% to $1.2643

- The Japanese yen was little changed at 149.69 per dollar

Cryptocurrencies

- Bitcoin fell 2.5% to $95,353.61

- Ether fell 3% to $3,598.72

Bonds

- The yield on 10-year Treasuries advanced three basis points to 4.20%

- Germany’s 10-year yield declined five basis points to 2.03%

- Britain’s 10-year yield declined three basis points to 4.21%

Commodities

- West Texas Intermediate crude was little changed

- Spot gold fell 0.3% to $2,636.28 an ounce

This story was produced with the assistance of Bloomberg Automation.

©2024 Bloomberg L.P.

KEEPING THE ENERGY INDUSTRY CONNECTED

Subscribe to our newsletter and get the best of Energy Connects directly to your inbox each week.

By subscribing, you agree to the processing of your personal data by dmg events as described in the Privacy Policy.

More oil news

Oil Rises With Focus on China’s Economy, OPEC+ Supply Meeting

South Korea’s Exports Regain Momentum on Steady Chip Demand

Canada’s Trudeau Holds Crucial Meeting With Trump at Mar-a-Lago

S&P 500 Rises for a Second Week; Yields Drop: Markets Wrap

Oil Little Changed in Thin Trading After OPEC+ Delays Meeting

GeoPark acquires Repsol’s Colombian oil and gas assets for $530 million

Oil Little Changed in Thin Trading Ahead of Key OPEC+ Meeting

ExxonMobil reports $8.6 billion Q3 2024 earnings, hits record 3.2M barrels/day production

Alberta Prepares to Fight Trudeau Cap on Oil and Gas Emissions