Geely, Xpeng, Xiaomi Boosted by Strong Vehicle Sales Amid Threats From EU Tariffs

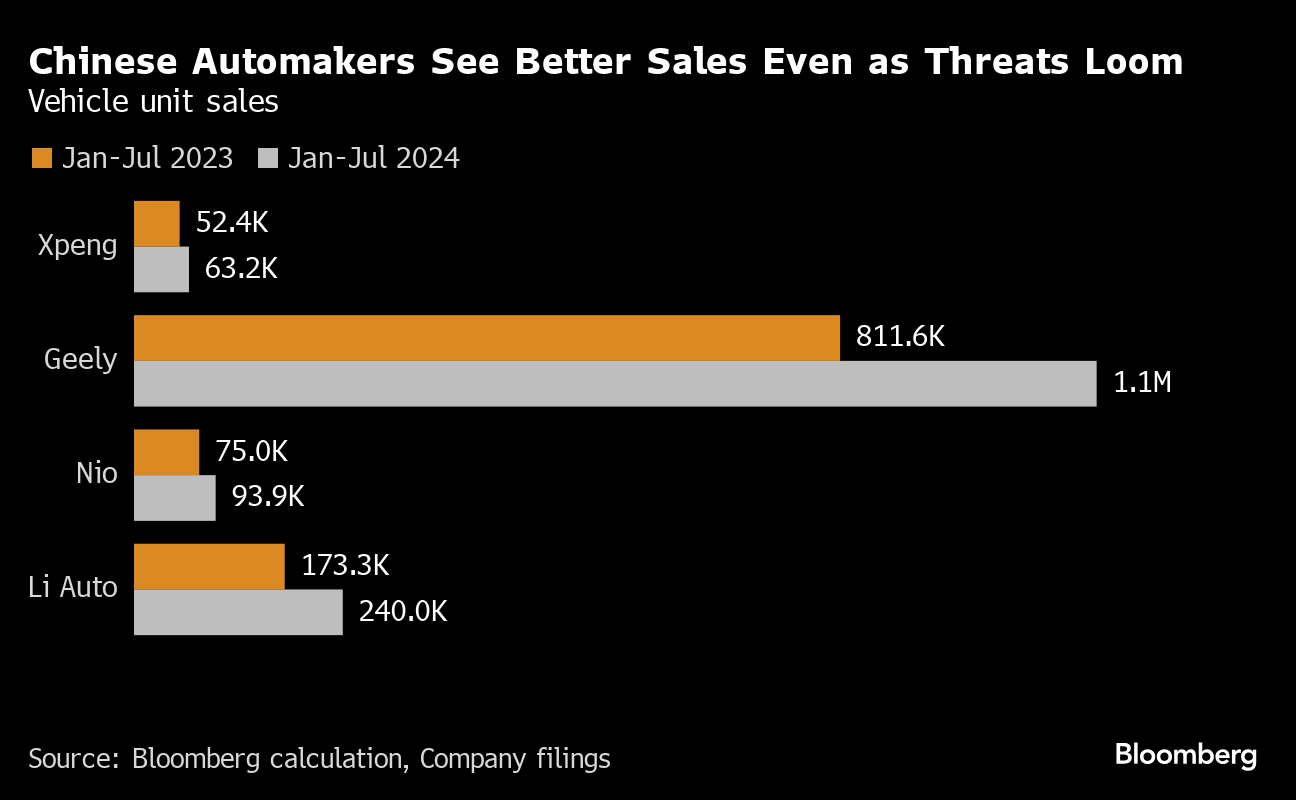

(Bloomberg) -- Chinese automakers including Xpeng Inc., Geely Automobile Holdings Ltd. and Xiaomi Corp. should all report higher vehicle sales, though challenges remain as competition heats up and the European Union moves ahead with tariffs.

The EU is hiking tariffs on EVs made in China by as much as 48%, citing subsidies that harm the bloc’s carmakers that have been struggling to keep up with China’s new generation of green car manufacturers. Chinese EV makers including Geely are responding by working with European partners to bypass tariffs.

Xiaomi’s EV sales are expected to reach 27 billion yuan ($3.8 billion) in 2024, with sales of 100,000 to 120,000 units, according to Bloomberg Intelligence. “China’s burgeoning EV market could become Xiaomi’s key growth engine in the next few years,” it said.

In the gaming arena, NetEase Inc. probably saw lackluster results as it works to deliver its next big video game title. Its long-term overseas growth strategy will likely continue to face difficulties this year, BI said.

Highlights to look out for:

Tuesday: Xpeng (XPEV US) is poised to report another quarterly net loss. SUV models likely led volume gains, while its most expensive model saw weaker sales. Technology-service revenue from Volkswagen AG was likely its key earnings driver amid lackluster automotive gross profit, BI said. A meaningful sales recovery will depend on its launch of a new EV model, though the margin upside looks limited given its affordable prices, BI added.

- Kuaishou Technology (1024 HK) has probably reached a plateau with its earnings growth as it sees more intense competition and slowing growth in China’s live-streaming e-commerce sector, said BI. Revenue for the live-streaming segment fell 14% in the second-quarter amid weak consumer sentiment, estimates show, while second-quarter adjusted net income was little changed sequentially.

Wednesday: Xiaomi’s (1810 HK) second-quarter sales likely surged 29%, while adjusted net income declined 5.6%, consensus shows. Higher-than-expected orders for its first EV model will likely boost sales by as much as 10% this year, though the launch will be a drag on margins. Currency tailwinds likely helped overseas sales growth and margins, BI said.

- Geely Automobile’s (175 HK) first-half earnings probably jumped with an improved product mix as shipments and exports surged, BI said. Price competition will remain challenging in the second half. Watch for comments on subsidiary Zeekr looking into building EVs in Europe to avoid EU tariffs.

- HKEX’s (388 HK) second-quarter profit was probably helped by gains in commodities, cash equities and derivatives revenue, BI said. Consensus is for a 9.1% increase in adjusted net income. The exchange might also see a sequential rebound in interest and investment incomes due to larger interest-earning assets, while as many as three large IPOs could be launched later this year, BofA Securities analysts said.

Thursday: Baidu’s (BIDU US) second-quarter adjusted net income is set to drop 16%, dragged down by lackluster advertising growth and rising costs for artificial intelligence ventures, which offset underlying growth in the cloud business and contributions from Ernie Bot. Rising competition and slowing economic growth weighed on advertising growth, which was probably the weakest in six quarters, BI said. Its outlook remains highly challenged as AI ventures are expected to be unprofitable for the next three years, BI added.

- NetEase’s (NTES US) adjusted profit may contract 11% amid ongoing regulatory constraints in the gaming industry in China. The firm may struggle to replicate the success of that boosted sales last year, analysts at BI said. The performance of the mobile version of unveiled in July, will have met investor expectations, analysts at Citi said.

- Bilibili’s (BILI US) increased advertising revenue from its expanding user base should have helped it narrow quarterly losses, consensus shows. That should help it turn profitable in the current third quarter, with analysts at Citi expecting better revenue from to play a key role. Momentum on online advertising and trends will be in focus on the earnings call, given management has said the advertising growth rate would be above the industry level in the medium term, analysts at Jefferies said.

©2024 Bloomberg L.P.

KEEPING THE ENERGY INDUSTRY CONNECTED

Subscribe to our newsletter and get the best of Energy Connects directly to your inbox each week.

By subscribing, you agree to the processing of your personal data by dmg events as described in the Privacy Policy.

More utilities news

EDF Profit Falls as Power Prices Retreat and Income Taxes Climb

Centrica Shares Surge on £4 Billion Investment Plan, Buybacks

Orano Says Rising Uranium Price May Revive Mining Projects

ADNOC Distribution and TotalEnergies celebrate two years of TEME joint venture in Egypt

Mars Joins With Fonterra to Cut New Zealand Farm Emissions

European Gas Prices Hold Near €50 With Supply Fears Easing

UK’s First New Nuclear Site Since the 1970s Begins Licensing

Scholz Leaves Germans With Worst Economic Blues in a Generation

Thames Water Takes Business Plan Dispute to Markets Watchdog