Wood Mackenzie: Chinese OEMs sweep the global wind podium for the first time

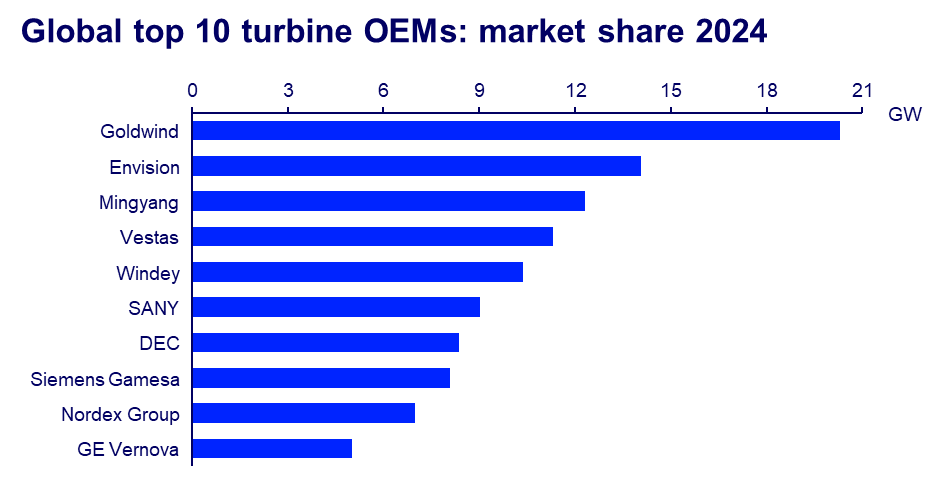

Wood Mackenzie's latest report on global wind turbine original equipment manufacturers (OEMs) reveals that Chinese companies dominated the market in 2024, with Goldwind, Envision, and MingYang securing the top three positions globally for the first time.

Key findings:

- Goldwind maintained its lead for the third consecutive year, installing 20 GW – a more than 20% increase on 2023 and more than 60% increase on 2024.

- Five OEMs installed double-digit GW for the first time, with Chinese manufacturers benefiting from robust domestic demand and Vestas dominating markets outside China.

- The Chinese market grew by almost 12% year-over-year to a record more than 80 GW, accounting for more than 60% of annual connected capacity globally.

- Installations outside China declined by 9% year-over-year, impacting Western OEMs.

Note: Wood Mackenzie bases its analysis on grid-connected capacity in all wind markets, except for China and Vietnam

Note: Wood Mackenzie bases its analysis on grid-connected capacity in all wind markets, except for China and Vietnam

Endri Lico, Principal Analyst at Wood Mackenzie, said: "The Chinese trio of Goldwind, Envision, and MingYang have captured the top global market share positions, marking a significant shift in the wind turbine manufacturing landscape. This is driven by China's booming domestic market, which shows no signs of cooling off in the near-term."

Despite record installations and orders, Chinese OEMs saw a drop in profitability due to intense competition and component oversupply. In response, they have agreed to maintain healthy competition, resulting in a price rebound in Q4 2024.

Western OEMs faced mounting pressures, with connections outside China dropping below 40 GW, the lowest since the COVID-19 pandemic. Vestas maintained its leading position outside China, connecting more than 10 GW in 2024, followed by Siemens Gamesa and Nordex.

"Western OEMs are adapting to the challenging market conditions by focusing on their core markets, restructuring their manufacturing footprint, increasing outsourcing from the East, divesting non-core activities, simplifying their product portfolios. More than anything, the Western OEMs exercised commercial discipline," Lico added.

Siemens Gamesa dominated offshore wind in a year where delays curbed connections. Global grid-connected offshore wind capacity declined in 2024 despite an all-time high being connected outside China. The subdued deployment in 2024 is due to both stop-and-go policies and delays.

China’s increased share of the global market and the transition to next generation offshore wind turbines increased both the spread of turbines deployed but also the weighted average turbine rating across the globe by 18% in 2024 compared with 2023.

KEEPING THE ENERGY INDUSTRY CONNECTED

Subscribe to our newsletter and get the best of Energy Connects directly to your inbox each week.

By subscribing, you agree to the processing of your personal data by dmg events as described in the Privacy Policy.